Pinnacle Apartment Sale Moves Ahead Despite New York City Objection

An auction for roughly 5,500 rent-regulated apartments takes place on Thursday after a bankruptcy judge rejected the city’s request to delay it

The bankruptcy sale of Pinnacle Group’s rent-regulated apartment portfolio is expected to generate losses north of $100 million for its mortgage lender, highlighting a continued devaluation in New York City apartments since the 2019 regulatory overhaul.

Flagstar Bank originally extended $564 million in mortgage loans secured by the portfolio of more than 5,000 units. Under the approved sale to a real-estate investment firm, Summit Properties, the bank will remain the lender, but the mortgage balance will be reduced to $338.5 million. As Pinnacle’s largest secured creditor, Flagstar is expected to receive most of Summit’s $113 million cash contribution for the purchase. But even after applying that cash, Flagstar is expected to incur a loss of more than $100 million on the loan.

Flagstar’s loss reflects an erosion in asset valuation of New York City’s rent-stabilized apartment properties following the enactment of the Housing Stability and Tenant Protection Act of 2019. The legislation put restrictions on landlords’ ability to increase rents, contributing to lower income growth expectations.

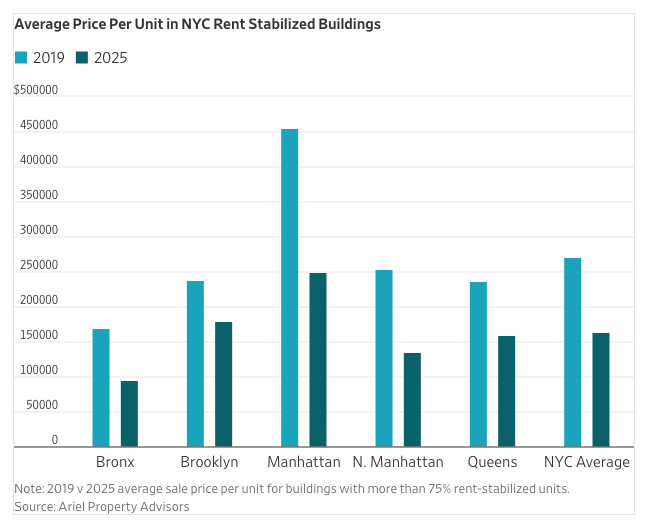

The average unit sale price for buildings with more than 75% rent-stabilized apartments in 2025 declined by roughly 40% below 2019 levels, according to Ariel Property Advisors, a commercial real-estate advisory firm in New York City. Declines were more pronounced in Northern Manhattan, Manhattan, and the Bronx, where values fell by 47%, 45%, and 44%, respectively.

Consistent with these market trends, the $451 million sale price for the Pinnacle portfolio represents an approximately 45% drop from the $826 million valuation previously carried on the company’s balance sheet.

Adding to the problem, a rise in rent arrears in post-pandemic has drained cash flow, and high interest rates have made refinancing harder, according to Greg Corbin, president of Northgate Real Estate Group.

Corbin, whose firm specializes in the sale of bankrupt assets, estimates that at least half of New York’s roughly 20,000 predominantly rent-stabilized buildings are now financially troubled. “I can’t imagine that any more than 50% of them, as a conservative number, are healthy,” said Corbin.